By Andrew Stein

These cost estimates are from the Vermont Campaign for Health Care Security Education fund, which helps enroll Vermonters in state subsidized insurance programs, like Catamount and VHAP. These estimates are based on the shift of annual health insurance costs for lower income Vermonters when the exchange takes place, and they include federal subsidies.

Lawmakers have frequently referenced these numbers in recent months, and they refer to the maximum amount Vermonters at these income levels would pay if they hit their out of pocket limits for a given year.

When the Green Mountain Care Board approved the core insurance plans for the state’s health benefit exchange, board members raised concern that the new insurance marketplace would leave some of Vermont’s most vulnerable residents in a precarious disposition.

Several key lawmakers say they must deal with the impact of the fiscal fallout of the exchange on thousands of low-income Vermonters who now receive subsidized health care and will face higher out of pocket costs in the new system.

“Front and center we need to continue to work on transition issues for people who are currently in VHAP (the Vermont Health Access Plan) or Catamount assistance and are moving into the health exchange,” said Rep. Mike Fisher, chair of the House Health Care Committee. “There are segments of that population for whom I’m concerned.”

Exactly how many of these Vermonters will receive government aid at current rates is unknown.

Gov. Peter Shumlin has acknowledged that some Vermonters will face steeper premiums and deductibles, but he told reporters recently he didn’t think the state had the money to make up the estimated $18 million difference.

The exchange, Vermont Health Connect, is slated to go into full effect on Jan. 1, 2014. At that time, Vermonters above 133 percent of the federal poverty line who do not work for businesses with 51-plus employees will be required to enter the exchange. That includes roughly 17,000 individuals now covered by the state-subsidized health insurance plans Catamount and VHAP.

If a person or family eligible for the exchange chooses not to buy health insurance, they will face tax penalties. But such disincentives might not be enough to convince some people to shell out more for less coverage.

Peter Sterling is director of the non-profit Vermont Campaign for Health Care Security and Education Fund, which helps to enroll Vermonters in Catamount and VHAP. He speculates that sending lower income Vermonters into the exchange with lesser coverage will deter them from participating.

“In the exchange it’s clear that all enrollees in Catamount and VHAP, who have to enter the exchange will pay significantly more in out-of-pocket costs than they do now,” said Sterling. “The exchange is not a good deal for these Vermonters, and I foresee a lot of problems getting them to enroll in the exchange.”

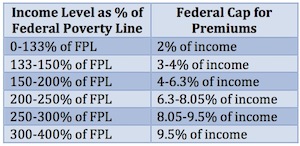

To figure out how much more these Vermonters might pay for health insurance, Sterling and his crew at the education fund ran the numbers. Although the Green Mountain Care Board won’t approve insurance premiums for the exchange until this summer, Sterling and his team used premium caps mandated by the federal Affordable Care Act. They also used the annual 2013 out of pocket limits set by the federal government.

This chart shows the sliding income scale for premium caps set by federal subsidies under the Affordable Care Act.

According to education fund calculations, an individual making about $28,000 a year, or 250 percent of the federal poverty line, would pay more than $5,000 annually in the exchange if he or she reaches the out-of-pocket maximum. Currently, an individual enrolled in Catamount would only pay about $1,900 under such circumstances.

A couple that makes a combined $45,000 a year, or 300 percent of the federal poverty line, can expect to pay almost $10,000 a year more than they do now, if they hit their out-of-pocket maximum. Right now they would pay roughly $7,000 between premiums and out-of-pocket costs; under the exchange they would pay almost 40 percent of their annual income (see figure 1).

At the board’s meeting last month, Department of Vermont Health Access Commissioner Mark Larson said that the state expects to save $10 million to $15 million on those Catamount and VHAP clients it will no longer subsidize. Currently, the state pays roughly 45 percent of their benefit, while Medicaid pays the rest.

Donna Sutton Fay, an advocate for the education fund, says those savings should be applied to the $18 million gap in benefits for low-income Vermonters. “It’s a little bit troubling because the $18 million the governor is using … is not that different from the amount the state is saving,” Sutton Fay said. “When the governor talks about the state not having that money, it seems like those savings should be going to those people who are already enrolled in those subsidized programs.”

Larson and Robin Lunge, Shumlin’s head of health care reform, said the state is not finished assessing the numbers. After Shumlin’s budget address in January, they plan to present legislators with final numbers and suggestions for dealing with this situation.

“There are a number of ups and downs in the DVHA budget in 2013, and so we’re trying to holistically look at that before we come up with a final proposal for this or anything else in the 2014 budget,” said Lunge.

One of the ups on the expenditure side of the state’s budget will come from a shift in coverage for Vermonters earning 100 percent to 133 percent of the federal poverty line. The Affordable Care Act gives Vermont the opportunity to enroll these individuals in the Medicaid program when the exchange starts. This move gives those VHAP enrollees better coverage, but it costs the state more. Currently, Medicaid only covers Vermonters up to 100 percent of the poverty line with some exceptions.

Lunge also argues that the state must look to the future, as the Catamount model might not be the most efficient way to provide coverage. Everyone on Catamount has the same annual deductible. The Affordable Care Act, on the other hand, will create a sliding scale to determine how much people will pay in out-of-pocket costs.

“It would not make sense to go back to the old Catamount model as one set of deductibles because that doesn’t match what the federal cost-sharing subsidy would do,” said Lunge. “That would create a confusing system for people.”

The cost-sharing subsidy limits the maximum amount that people will pay out of pocket in an individual year.

Robin Lunge, director of health care reform for the Shumlin administration, updates the Vermont Health Access Oversight Committee Wednesday on the progress of setting up a health benefits exchange where Vermonters will purchase health insurance. VTD/Alan Panebaker

For income levels at 100 percent to 200 percent of the poverty line, the federal bill calls for a two-thirds reduction in the out-of-pocket maximum; for 200 percent to 300 percent of the federal poverty line, the act requires a 50 percent reduction in that maximum; and for people earning 300 percent to 400 percent of the poverty line, the out-of-pocket maximum will be reduced by one-third.

Additionally, a federal tax credit caps the amount people who make up to 400 percent of the federal poverty line will pay for premiums using a scale that is income dependent. As Fisher understands the situation, these tax credits will be issued as advances for the first year of the exchange.

The reason why Catamount is ending, said Lunge, is that it’s a private insurance product that won’t fit the federal requirements of the Affordable Care Act when the exchange is implemented in 2014.

For the roughly 20 percent of VHAP recipients who are not set to move into Medcaid, it’s a different story.

In theory, said Lunge, the state could ask the feds to allow the 7,000 individuals to enroll in Medicaid, but it would cost the state more.

“We’d be asking Vermonters to pay for something through state taxes that they’ve already paid for through their federal taxes,” she said. “Financially it’s better for the state if folks move into the exchange with the federal premium tax credit and cost-sharing subsidy.”

Even with these federal subsidies, Vermonters at 133 percent to 300 percent of the federal poverty line are looking at sharp increases in health insurance.

More uninsured Vermonters?

Fisher said he is particularly worried about the level of coverage Vermonters between 250 percent to 300 percent of the poverty line will receive.

“There’s a set of people who I’m concerned about who are above 250 percent of the federal poverty line for whom the federal supports may land them in coverage levels that I’d call underinsured, where their co-pays and deductibles are a high percent of their income,” he said.

“We have an estimated 160,000 underinsured Vermonters,” Fisher added. “I want to shrink that number.”

[5]

Peter Sterling, executive director of Vermont Campaign for Health Care Security Education Fund. VTD/Alan Panebaker

Fisher and Sen. Claire Ayer, chair of the Senate Health Care Committee, both said they know loose change will be a hot commodity for the Legislature this session, as the state grapples to fill holes in the General Fund budget.

“We’re going to have to be pretty careful and look at budgets,” said Ayer. “Our job is going to be to make sure the health system proceeds and that human services aren’t too adversely affected.”

Lunge said that state subsidies for health insurance fall under three umbrellas: benefits to lower premiums, cost sharing, and the yearly out of pocket maximum. If she had to pick and choose, Lunge would prioritize benefits for premiums because they would encourage more people to purchase insurance.

“If people don’t feel like premiums are affordable, they don’t (buy) insurance,” she said. “That’s a primary concern because some insurance is better than no insurance. There’s clear research that shows a connection to better health outcomes if you have any insurance over no insurance.”

Lunge said the state is exploring whether it can appropriate extra Medicaid dollars to such subsidies via the state’s federal waiver for its global commitment program, which allows it to use such funds for a broader range of health care initiatives. The state will apply for a new waiver in 2013, and Lunge said the state plans to include a proposal for such subsidies in that application.

When everything is taken into account, said Fisher, getting people the coverage they need will help Vermont on health care and fiscal levels. The question is whether the state has the funds up front to do that.

“This is a big budget question, and we don’t know the details yet,” he said. “We need to figure out what resources we have.

“The goal is to help ensure that Vermonters have access to affordable care so that they can get the health care they need. We know that if people get the care they need when they need it, it saves us money in the long run.”